In recent years, several changes in the compliance landscape, including ASC 606 / IFRS 15 on Revenue Recognition and ASC 842 / IFRS 16 on Lease Accounting, have significantly altered the requirements for what data must be disclosed and how disclosure reporting is handled.

Many companies are still struggling with complex reporting. Some companies believe that a purpose-built solution for complying with the standards is not easily available and implementing can be complex for some scenarios.

Others have chosen to use “brute force” solutions such as spreadsheets or alleged cloud solutions that integrate with their ERP only to find it just doesn’t work.

In recent years, several changes in the compliance landscape, including ASC 606 / IFRS 15 on Revenue Recognition and ASC 842 / IFRS 16 on Lease Accounting, have significantly altered the requirements for what data must be disclosed and how disclosure reporting is handled.

Many companies are still struggling with complex reporting. Some companies believe that a purpose-built solution for complying with the standards is not easily available and implementing can be complex for some scenarios.

Others have chosen to use “brute force” solutions such as spreadsheets or alleged cloud solutions that integrate with their ERP only to find it just doesn’t work.

According to SEC officials in ASC 606/ IFRS 15 Disclosure following issues has been highlighted

In ASC 842/IFRS16 Disclosure, the SEC has highlighted following issues

According to SEC officials in ASC 606/ IFRS 15 Disclosure following issues has been highlighted

In ASC 842/IFRS16 Disclosure, the SEC has highlighted following issues

“What’s Get Measured: Gets Managed”

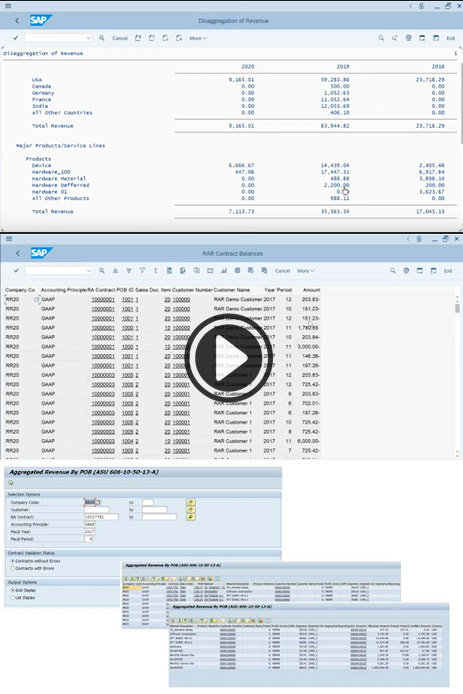

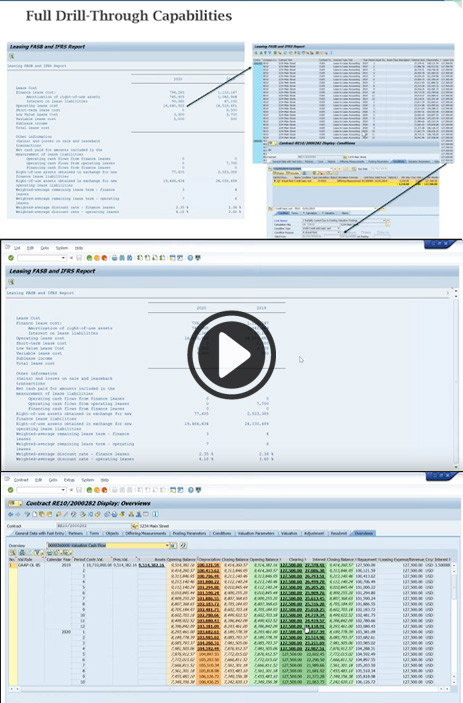

In order to deliver the full range of information in real-time and with agile manipulation of data for analysis, finance users need analytics dashboards optimized for visualization, along with flexible reports and the ability to drill-through into front-line applications such as SAP Revenue Accounting and Reporting (RAR), SAP Contract Lease Management (CLM) and to drill back to General Ledger detail.

In addition, the analytics and disclosure reporting tools must be able to seamlessly scale up for handling increasing large data sets, with real-time modeling and what-if scenarios.

Throughout the recent changes in Revenue Recognition and Lease Accounting compliance requirements, Bramasol has been at the forefront of implementing targeted SAP solutions and developing comprehensive disclosure reporting methodologies that are integrated with advanced analytics capabilities.

Bramasol have recently released an update to Analytics-Driven Disclosure Reporting Packages for RevRec and Lease Accounting that incorporate a range of significant improvements to functionality, performance and scalability.

“What’s Get Measured: Gets Managed”

In order to deliver the full range of information in real-time and with agile manipulation of data for analysis, finance users need analytics dashboards optimized for visualization, along with flexible reports and the ability to drill-through into front-line applications such as SAP Revenue Accounting and Reporting (RAR), SAP Contract Lease Management (CLM) and to drill back to General Ledger detail.

In addition, the analytics and disclosure reporting tools must be able to seamlessly scale up for handling increasing large data sets, with real-time modeling and what-if scenarios.

Throughout the recent changes in Revenue Recognition and Lease Accounting compliance requirements, Bramasol has been at the forefront of implementing targeted SAP solutions and developing comprehensive disclosure reporting methodologies that are integrated with advanced analytics capabilities.

Bramasol have recently released an update to Analytics-Driven Disclosure Reporting Packages for RevRec and Lease Accounting that incorporate a range of significant improvements to functionality, performance and scalability.

This new release includes significant improvements to both functionality and performance, including the following.

Revenue Recognition Disclosure Reporting:

Revenue Recognition Disclosure Reporting:

Lease Accounting Disclosure Reporting:

Lease Accounting Disclosure Reporting: